After the announcement of the Q4 results of Tata Motors on May 10th, the stock price of the company saw a sharp decline today (Monday). Tata’s share price opened downside at ₹1005 per share on the National Stock Exchange (NSE) and touched an intraday low of ₹947.20 per share within a few minutes. The stock overall recorded an intraday loss of more than 9 per cent on Monday (today).

Tata Motors Q4 results

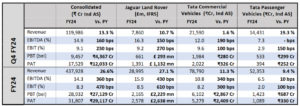

The Q4 FY24 results show that the net profit more than tripled. The company showed a 222 per cent year-on-year growth in its net profit. The net profit jumped to ₹17,407 crore, while the Revenue from operations increased to ₹1.2 lakh crore by 13 per cent.

The operating profit increased by 81 per cent at ₹9,754.66 crore, while the operating margin increased by 60 per cent to 8,13 per cent.

The EBITDA for FY24 stands at 14.9 per cent and the EBT stands at 9.1 per cent.

Why did the stock price fall?

Regarding the fall in share price after the release of Q4 results, Chirag Jain, Senior Research Analyst at Emkay Global Financial Services said, “Tata Motors Q4 results 2024 were muted with limited margin expansion across businesses despite higher volumes. The company remains cautiously optimistic across businesses, with H1 expected to be weaker and the premium luxury segment seen as resilient amid overall emerging demand concerns.

While deleveraging progress continues, we believe the best may be behind for all businesses amid i) declining orderbook, normalizing mix, and higher customer acquisition costs at JLR, with FCF generation to normalize; ii) flattish growth outlook for domestic CV space; and iii) moderating India PV outlook (though TTMT to outperform on new launches). FY25E/26E EPS is largely unchanged (we build-in consol. revenue/EBITDA CAGR of 7/8% over FY24-26E).”

Motilal Oswal downgraded to a ‘neutral’ rating

While maintaining a ‘neutral’ rating on Tata Motors stock prices, Motilal Oswal report said, “Tata Motors 4QFY24 result was operationally in line with our estimate as EBITDA margin expanded 30basis points QoQ to 14.2%. While there is no doubt that TTMT has delivered an extremely robust performance across its key segments in FY24, there are clear headwinds ahead that are likely to hurt its performance.”

‘Steady JLR business performance’

The Kotak Institutional Equities said that the EBITDA was below estimates, driven by weak domestic CV business performance. It generated FCF of Rs 26,900 crore in FY24, resulting in a sharp reduction in consolidated net debt and remains on track to become net cash by FY25E, it said.

“Overall, we expect the FY2025-26E performance to remain healthy, led by steady JLR business performance, driven by an improvement in mix and cost control measures, market share gain in the PV and CV segments and net cash balance sheet by FY25E,” it added with an ‘add’ rating with a fair value of Rs 1,100.

Nomura also downgraded the stock to ‘neutral’ from ‘buy’ but increased the target price to ₹1,141 as it said that the stock is in the fair value zone after a steady performance. “JRL may face demand risks, while PVs business will grow ahead of the industry with moderation in the commercial vehicle industry,” Nomura said.

JPMorgan is also bullish on the stock with an ‘overweight’ rating, increasing the target to ₹1,115, while Morgan Stanley downgraded the stock to ‘equal weight’ with a target price of ₹1,100.

{kind=link}

Comments 2